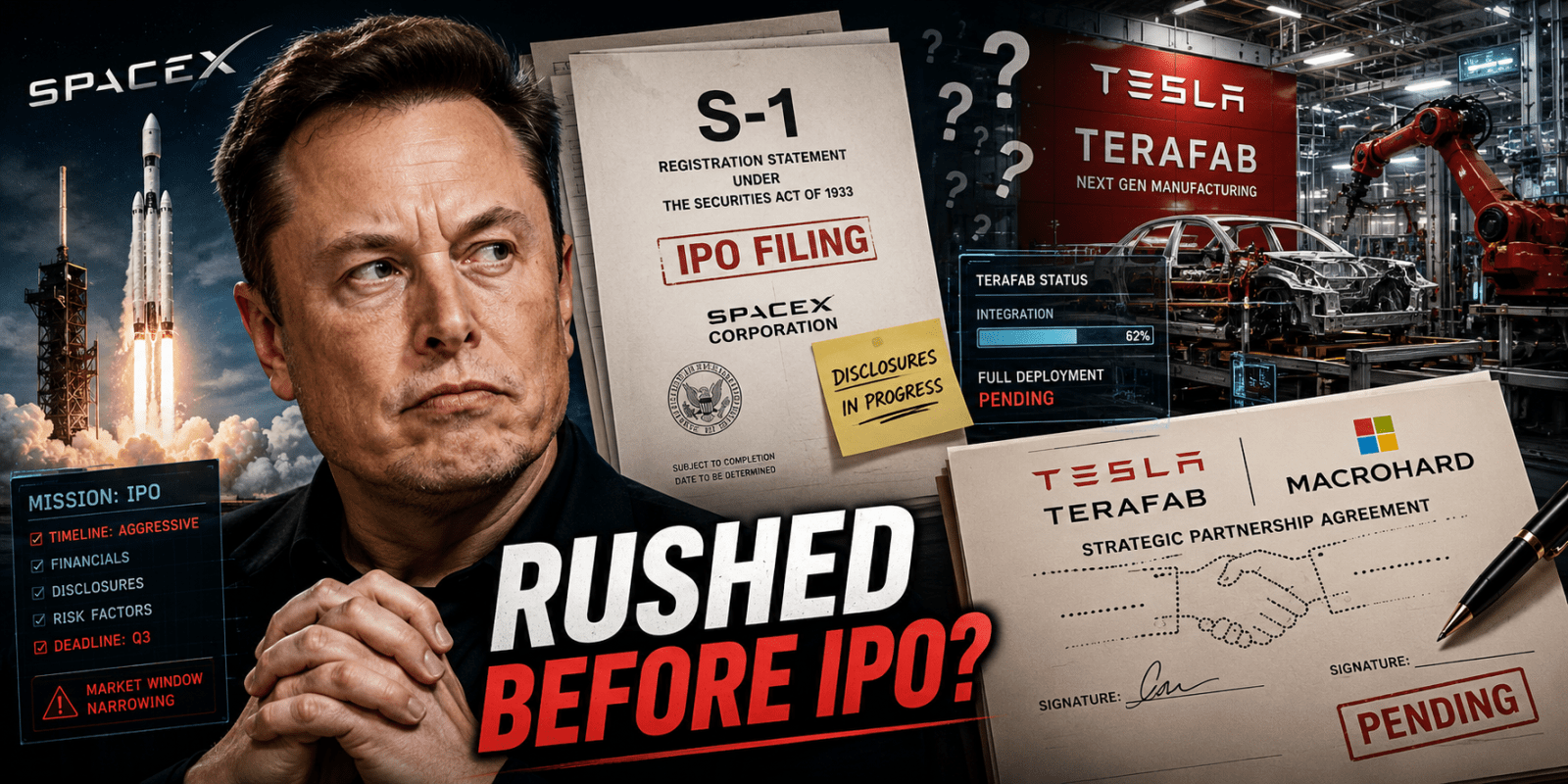

SpaceX filed its S-1 with the SEC today ahead of its blockbuster IPO, and buried in the 308-page document is a sobering reality check on the Tesla (TSLA) collaborations that Elon Musk has been hyping for months.

The legal language in SpaceX’s own filing reveals that both Terafab and Macrohard — the two major joint projects between Tesla and SpaceX — are in “very early stages” with no financial terms, no intellectual property rights, and no binding commitments finalized.

$650 million in related-party transactions

The S-1’s related-party transactions section quantifies just how financially intertwined Musk’s companies have become. In 2025 alone, SpaceX obtained $144 million in goods and services from Tesla — up from just $4 million in 2024. That 36x jump in a single year is striking.

But xAI’s Tesla tab dwarfs SpaceX’s. The former AI startup, which SpaceX absorbed in February 2026, purchased $506 million in goods and services from Tesla in 2025 and another $34 million in just the first two months of 2026. Those purchases are primarily Megapack battery storage systems powering xAI’s data centers.

Combined, Tesla received roughly $650 million from SpaceX/xAI entities in 2025. Tesla also holds 18,990,195 shares of SpaceX Class A common stock, less than 1% ownership, converted from its $2 billion xAI investment when SpaceX acquired xAI.

Tesla even started buying advertising on X, spending $4 million in 2025 after years of Musk insisting Tesla doesn’t advertise.

Terafab: “general framework” with no binding terms

When Musk announced Terafab in March 2026, he painted it as a transformative $25 billion chip manufacturing colossus — the world’s largest semiconductor facility, vertically integrating lithography, fabrication, and packaging under one roof.

SpaceX’s S-1 describes the ambition similarly, calling Terafab an initiative to produce “one terawatt of compute hardware each year” with two chip types — one for Tesla’s Optimus robots and vehicles, another for SpaceX’s orbital compute infrastructure.

But the legal disclosures tell a different story. SpaceX states it has agreed with Tesla on “a general framework for the future development of Terafab.” That’s it. A framework.

The filing then adds: “Any specific projects undertaken pursuant to this framework will be subject to separate negotiations and agreements (including any development timelines, milestones and capital expenditures) and have not yet been determined.”

The risk factors section goes further: “While we have a framework agreement with Tesla, neither Tesla nor Intel are obligated to remain a part of the project, and we may not enter into any such definitive agreements.”

And in the conflicts-of-interest disclosure: “Certain of these projects, including Macrohard and Terafab, are in the very early stages, as a result of which we and Tesla have not finalized a variety of details relating to our collaboration, including, but not limited to, financial terms, intellectual property rights, and the ultimate term of our collaboration.”

No financial terms. No IP ownership. No timeline commitments. No capital expenditure obligations. Neither partner is even required to stay.

As we noted when Intel joined the project, the reality of building a cutting-edge chip fab is a far cry from announcing one on social media. The S-1 confirms that gap.

Macrohard: ambitious claims, zero details

The other major Tesla collaboration disclosed in the S-1 is Macrohard, described as “an agentic AI platform designed to be capable of fully emulating digital workflows and augmenting human operation of computers — from coding and product development to management and entire business processes — using sophisticated autonomous agents.”

SpaceX says it expects Macrohard to “fundamentally transform how companies are structured and operate.” In the glossary, it’s described as a platform to “create a fully AI-operated software company.”

The filing says Macrohard is being developed “together with Tesla” and will benefit from running on “both state-of-the-art processors and cost efficient, next-generation Tesla processors.”

But as with Terafab, there are no disclosed financial terms, no IP ownership structure, no revenue-sharing arrangement, and no indication of whether this is a SpaceX product, a Tesla product, or a joint venture. The same “very early stages” language applies to both projects.

The timeline is suspicious

The pattern here is hard to ignore. Terafab was announced in March 2026. Intel was added in April 2026. The S-1 was filed in May 2026. Both Macrohard and Terafab appear prominently in the prospectus summary — the section designed to sell investors on SpaceX’s vision.

But SpaceX’s own lawyers had to disclose that none of these collaborations have binding terms. The risk factors explicitly warn that the projects may never materialize: “there can be no assurance that we will be able to achieve our objectives with respect to Terafab within the expected timeframes, or at all.”

Musk has a well-documented pattern of making grand announcements around capital-raising events. Tesla’s “Robotaxi” unveil came before a stock offering. The “Master Plan Part 3” preceded another. Now Terafab and Macrohard land conveniently in time for what could be the largest IPO in history.

Musk’s divided attention

The S-1 also includes a candid admission about Musk’s time: he “does not devote his full time and attention” to SpaceX’s businesses. The filing notes he “currently serves as Technoking and Chief Executive Officer of Tesla and is involved in other emerging technology ventures, including Neuralink and The Boring Company” and “previously served as Senior Advisor to the President of the United States.”

SpaceX does not carry key-person life insurance on Musk.

The charter also gives Musk broad latitude to pursue competing interests. SpaceX “renounces certain corporate opportunities” that may come to Musk, meaning he has no legal duty to bring business opportunities to SpaceX first. The same applies to Tesla — Musk and his affiliates are “not restricted from owning assets or engaging in businesses that compete directly or indirectly” with SpaceX.

Electrek’s Take

The SpaceX S-1 is a remarkable document. The biggest IPO in history is trying to list at almost 100x revenue and no profits. Mostly based on dubious, unproven industries, such as “data centers in space.”

Also, on one hand, it confirms the scale of financial entanglement between Musk’s companies — $650 million in transactions in 2025 alone, a pattern that has been accelerating rapidly.

On the other hand, the legal language around Terafab and Macrohard paints a picture that is starkly different from Musk’s public pronouncements. These are not done deals. They are concepts with a “general framework” and nothing more — no money committed, no IP allocated, no timelines agreed upon.

The timing raises obvious questions. Musk needed impressive narratives for the SpaceX IPO, and “world’s largest chip factory” and “AI platform that will fundamentally transform companies” certainly deliver on that front. But the S-1’s own risk factors essentially tell investors not to count on any of it happening.

It looks like Musk rushed to announce the Terafab project before SpaceX’s IPO without anything concrete.

With electricity rates climbing nearly 10% last year, home solar protects you against future rate increases. And with lease and PPA options, you can go solar with zero upfront cost and start saving immediately. If you want to find the best deal, check out EnergySage. It’s a free service with hundreds of pre-vetted installers competing for your business, so you save 20 to 30% compared to going it alone. No sales calls until you pick an installer. Get your free quotes here.

FTC: We use income earning auto affiliate links. More.

Comments